India Real Estate: Challenges and Opportunities presented by COVID-19 - II

- By Shwetha Pai and Venkatesh Panchapagesan

- September 07, 2020

Share This Story

Real Estate, Slowdown, Recovery, Liquidity

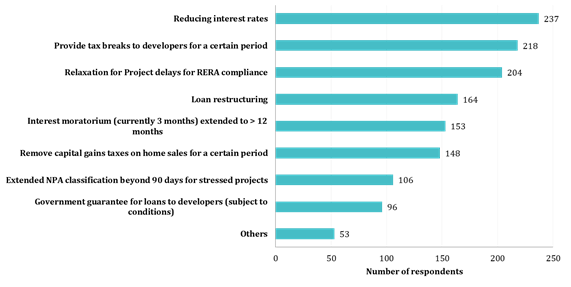

This is the second article in our series on the Impact of Covid-19 on the Indian Real Estate Sector. This series is based on a survey conducted by IIM Bangalore’s Real Estate Research Initiative (RERI) in April/May 2020 with the participation of 294 developers across India. For more details on the survey refer to click here. In our previous article, we highlighted the three challenges developers faced in their post lock-down recovery efforts, namely – resumption of sales, retention of labour and cost control. To read the first article in this series refer to click here. In this article, we will focus on the challenge of liquidity that has been plaguing the real estate sector for the last couple of years and has been further aggravated by the COVID-19 lockdown. The sector expected government intervention to address this key issue. According to our survey the top expectations of the respondent developers from the government are shown in the figure below.

Figure 1:Government intervention expected by real estate developers in response to COVID-19

The government on its part has given a massive relief package in order to boost the economy post the lockdown. The government’s relief measures for the real estate sector announced between April 2020 to August 2020 can be grouped under three major heads:

-

Increase liquidity in the system: Steps such as lowering interest rates, infusion of INR 15,000 crores in NHB (in two tranches) to improve long term funding requirements of NBFCs and HFCs, moratorium on all term loans for a period of 6 months and the recent announcement of a one-time loan restructuring.

-

Compliance under RERA and IBC: invoking force majeure1 clause under RERA and extending project registration and completion timelines by 6 months for all projects registered under RERA. Increasing threshold limit for Insolvency proceedings fro INR 1 L to INR 1 crore.

-

Reduction in taxes to boost housing demand: Reduction in stamp duty on affordable housing projects by states such as Karnataka (stamp duty reduced from 5% to 3% for properties valued less than INR35L and to 2% on properties valued less than INR 20L) and Maharashtra (stamp duty reduced from 5%-2% between September-December 2020 and to 3% from January to March 2021 in urban areas across price segments), reduction in TDS on sale of property by 25% and extension for filing GST and Income Tax.

All of the above steps have provided much-needed relief to the residential real estate sector, by addressing problems of liquidity, debt servicing, delay and demand at least for the short term. This article will address the trends that emerge in strategic decisions of developers to improve cashflows in the next 6-12 months.

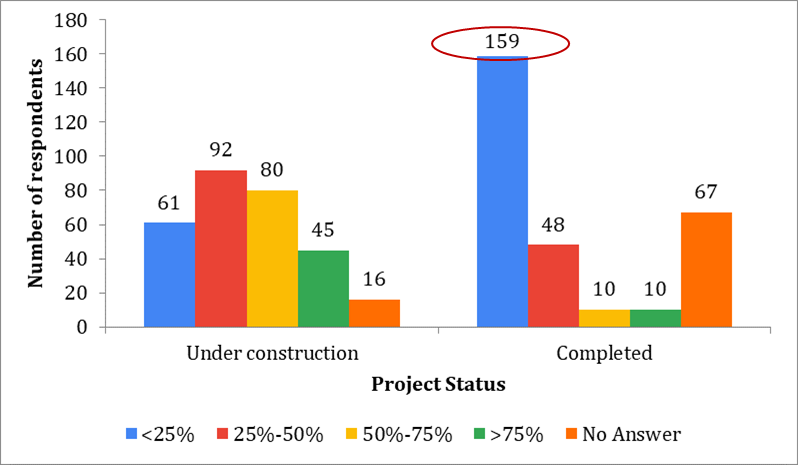

Firstly, residential developers are likely to refrain from new launches at least during the second half of FY 21. New launches in Q2 2020 dropped by 84% as compared to Q1 20202. Developers’ focus will now be on completing ongoing projects and reduction of unsold inventory3.

Figure 2: Distribution of respondents based on percentage of unsold inventory in under-construction and completed projects

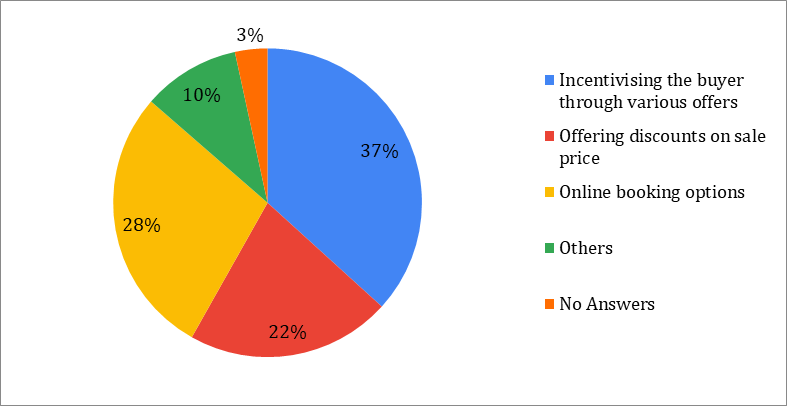

According to our survey, 54% of the respondents had 25% or less unsold inventory in their completed projects, in other words ready-to move in properties. The focus of these developers will be on sales of this inventory to help improve their cashflows. To achieve this, pricing is either going to be stable or at a discounted price as in the case of a few developers who are under severe liquidity stress. According to our survey, 22% of the survey respondents had considered a reduction in price. However, price reduction has its own challenges for both the buyers and sellers in terms of taxation.

Figure 3: Sales strategy post lock-down

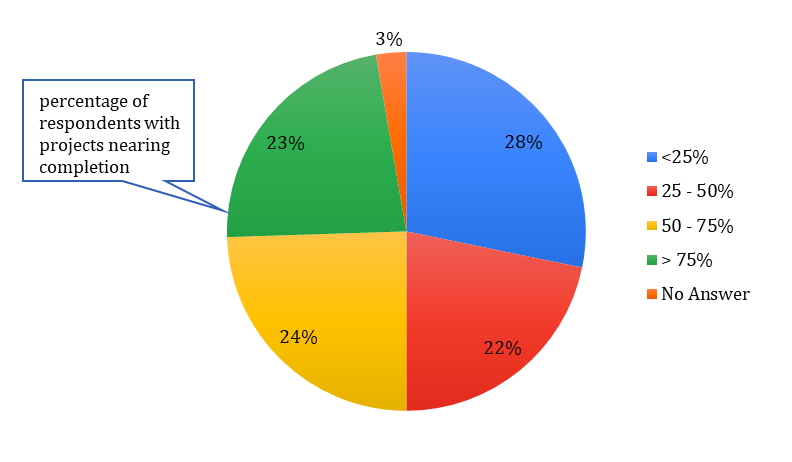

The third important concern is to finance construction of ongoing projects. One-time restructuring of loans for corporates and individuals, a recent step taken by RBI (in Auguest 2020), is expected to provide much needed respite to the real estate sector. On the supply side it will help developers impacted by COVID restructure their existing loans with a two year moratorium without classifying these loans as Non-Performing Assets (NPAs).This will help residential developers raise last mile funding for their projects stuck due to COVID-19. On the demand side, restructuring individual home loans will help buyers who are impacted by job loss and pay cuts to manage their EMIs. However, fresh lending to the sector from Banks and Non-Banking Finance Companies (NBFC) will remain subdued as their focus will be on restructuring of existing loans.

Figure 4: Distribution of under-construction projects under various stages of construction

In the absence of funds from Banks and NBFCs, developers will turn towards PE funds. Although PE funding in the real estate sector has reduced significantly in the first half of 2020, it is expected to recover in the coming months as these funds have sufficient dry-powder to invest, but are waiting to understand the full impact of this pandemic on asset valuations. While most PE funds may focus on assets such as data centres and warehouses, in the residential segment PE funds are expected to select projects that are nearing completion due to their low risk profile. According to our survey, 23% of the respondents had projects that were nearing completion (more than 75% complete). Alternative lenders such as Private Debt Funds and Special Situation Funds will be active during the next 12 months.

Finally, the next 12-18 months are also likely to witness a second round of consolidation (a first round of consolidation had started as a result of policy reforms such as RERA and GST and the NBFC crisis), where highly leveraged, small to mid-sized developers with large unsold inventory, poor execution capabilities, and most importantly, failed to invest in technology are likely to liquidate their assets at distressed valuations. IIMB RERI will conduct a second round of this survey in September 2020 to understand the impact of these policy measures on the sector.

Source:

1Force Majeure is defined as an event for which no party under a contract can be held accountable. Natural events such as an earthquake or a tsunami and human actions such as war, armed conflict fall under force majeure.

2Source: PropEquity, Q2 2020

3Unsold inventory refers to units launched/ under-construction but not sold as on April 2020.

Shwetha Pai

Venkatesh Panchapagesan